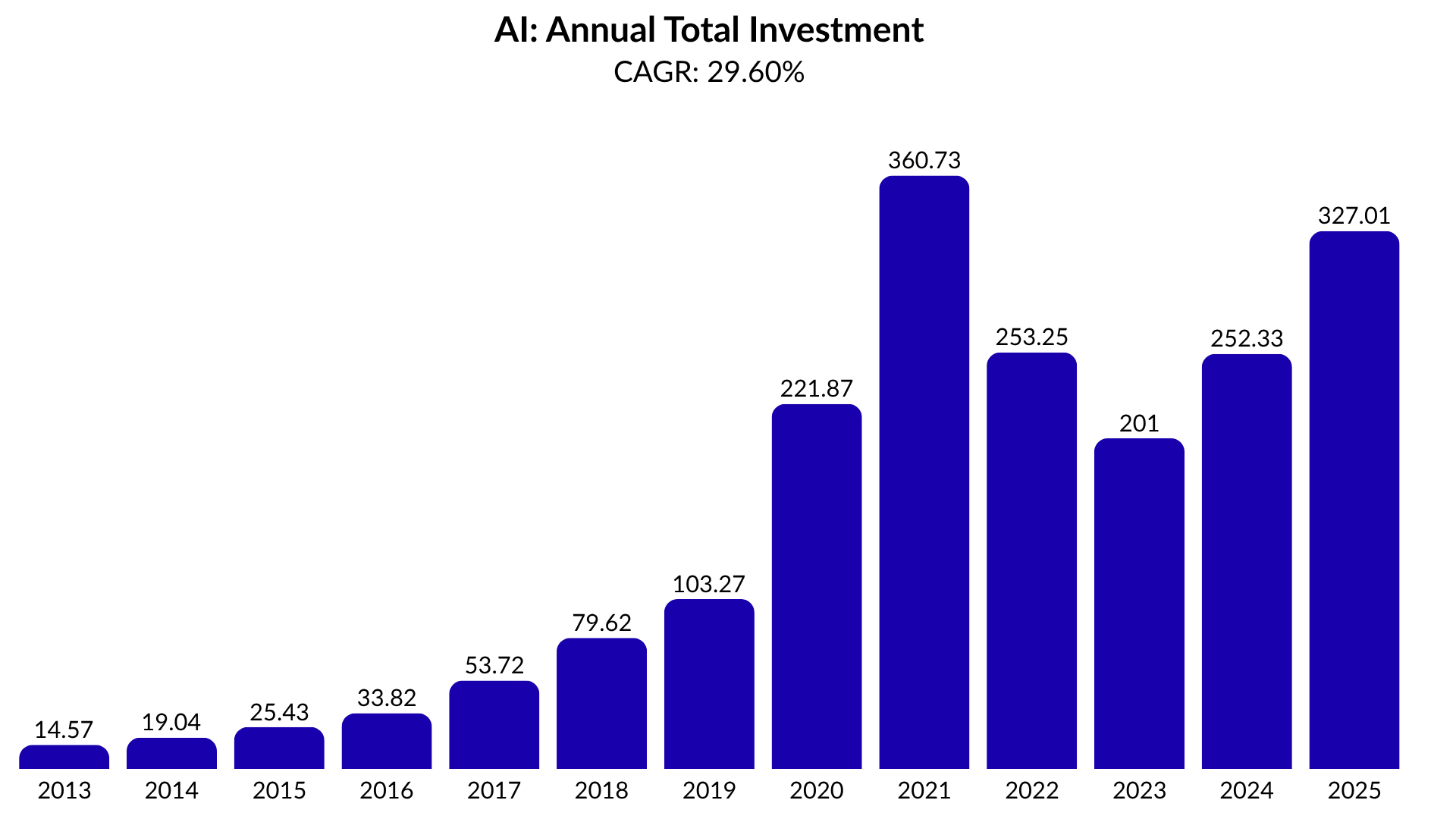

AI is increasingly becoming an infrastructure problem rather than a software problem. Global AI investment has increased from USD 14.6bn in 2013 to an estimated USD 327bn in 2025, while enterprise adoption has reached roughly 75% across major organisations. At this scale, the question is no longer whether AI demand exists. The more important question is whether the underlying infrastructure supporting AI can expand fast enough to meet future demand.

Energy may become one of the most important constraints behind long-term AI deployment. Data centres require substantial computing capacity, and computing capacity ultimately requires power generation. This article examines the relationship between AI investment, data centre expansion, and energy supply/demand within the United States. The objective is not to challenge the AI investment thesis, but to understand the infrastructure requirements and potential bottlenecks sitting underneath it.

Part 1: AI Is Not the Experiment Anymore

AI demand is no longer the primary uncertainty surrounding the industry. With global investment reaching hundreds of billions of dollars and enterprise adoption becoming increasingly widespread, AI has already achieved sufficient scale to create meaningful infrastructure requirements. The discussion therefore increasingly shifts away from software capability and toward the physical systems required to support future growth.

Source: Stanford, Quid, NP Estimates

AI investment has already reached infrastructure scale. Global corporate investment in AI increased from USD 14.57bn in 2013 to an estimated USD 327bn in 2025, implying a 29.6% CAGR over twelve years. More importantly, investment activity remained structurally elevated even after the 2021 peak rather than collapsing back to pre-cycle levels. Cumulative capital deployed into AI is likely approaching USD 2tn. At this scale, AI is no longer constrained by software capability alone.

Source: Mckinsey, Stanford, NP Estimates

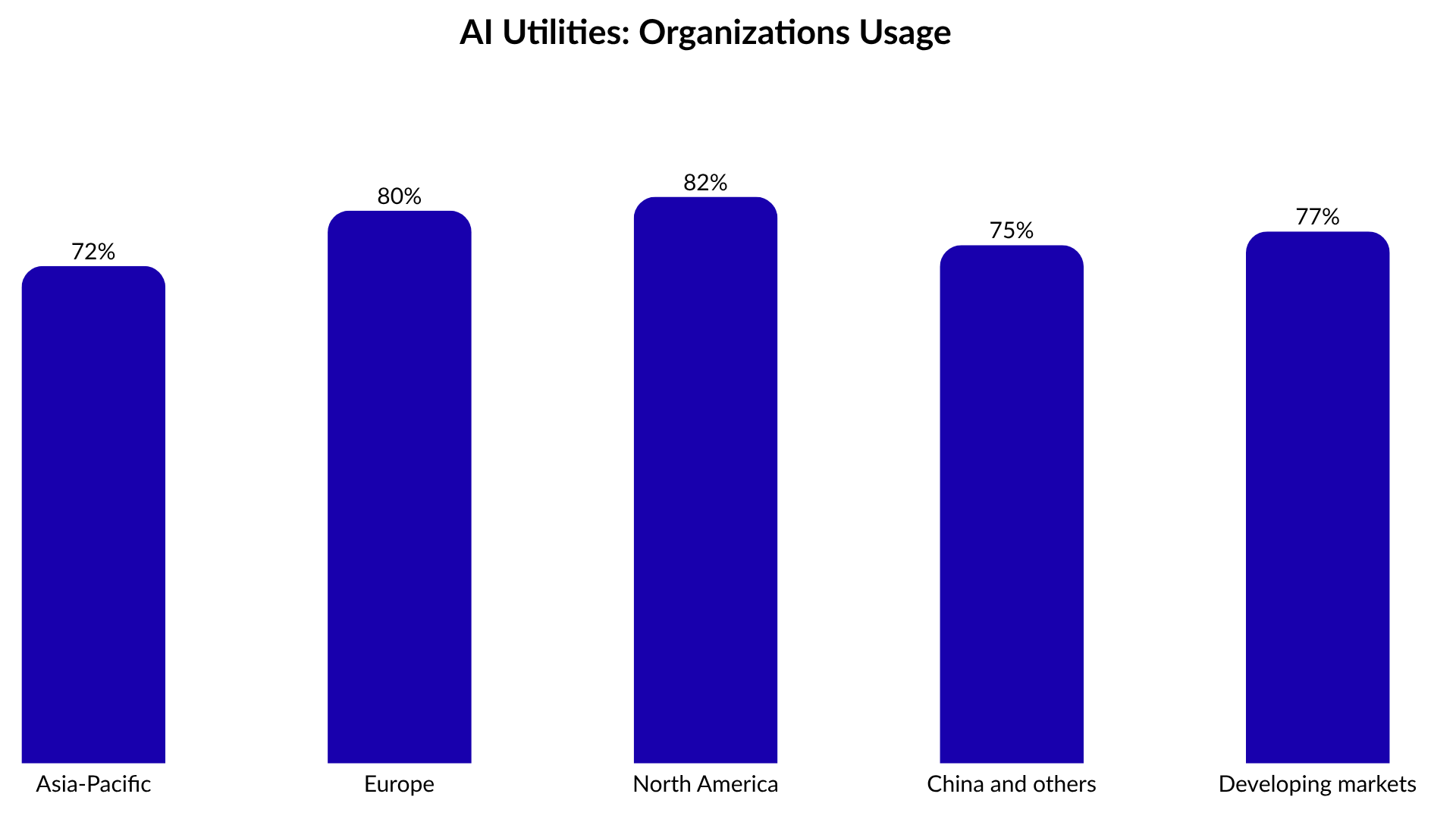

AI adoption has already become standard enterprise behaviour. Around 75% of organisations across major regions now use AI across functions including marketing, sales, operations, and risk management. At that level of adoption, AI demand stops being a software story and starts becoming an infrastructure problem. Large-scale deployment requires compute capacity, and compute capacity ultimately scales through data centres.

Part 2: Every Prompt Needs a Home

AI deployment ultimately depends on physical infrastructure. Most frontier AI companies operate through large-scale data centres, making compute capacity one of the key requirements behind continued AI adoption. As AI usage increases across the economy, data centre expansion increasingly becomes an infrastructure challenge involving power availability and capital investment. The growth of AI therefore depends not only on software innovation, but also on the ability to expand the physical systems supporting it.

Source: International Data Center Authority, NP Estimates

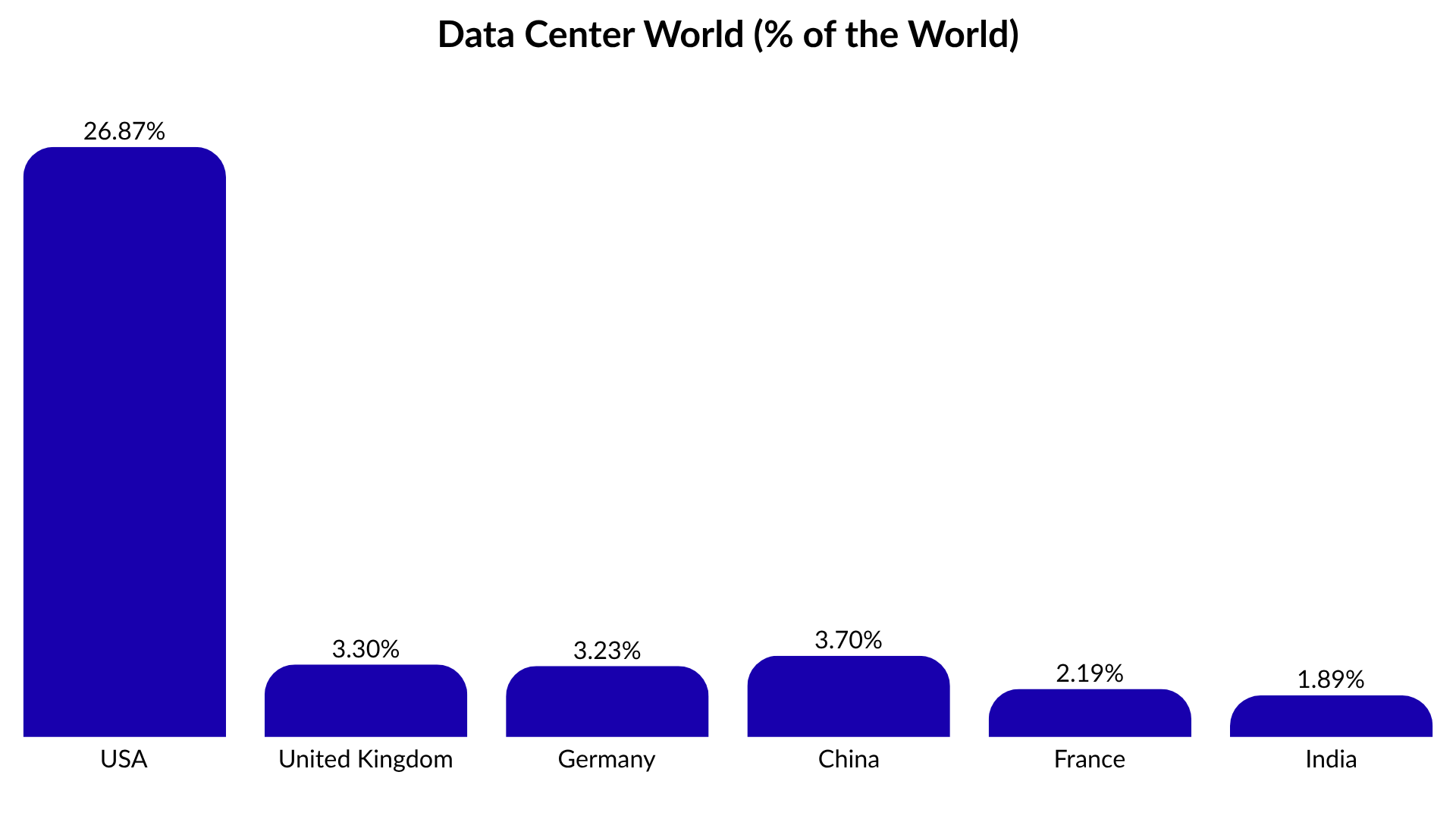

AI infrastructure is becoming increasingly dependent on US data centre capacity. Most frontier AI companies, including OpenAI, Anthropic, Google, Meta, and xAI, primarily operate through US-based data centres due to latency and compute requirements. The concentration is substantial. The US alone accounts for roughly 26.9% of global data centre capacity, materially larger than any other country. As AI deployment scales further, data centre expansion increasingly becomes an energy and infrastructure problem.

Source: IEA, US Department of Energy, NP Estimates

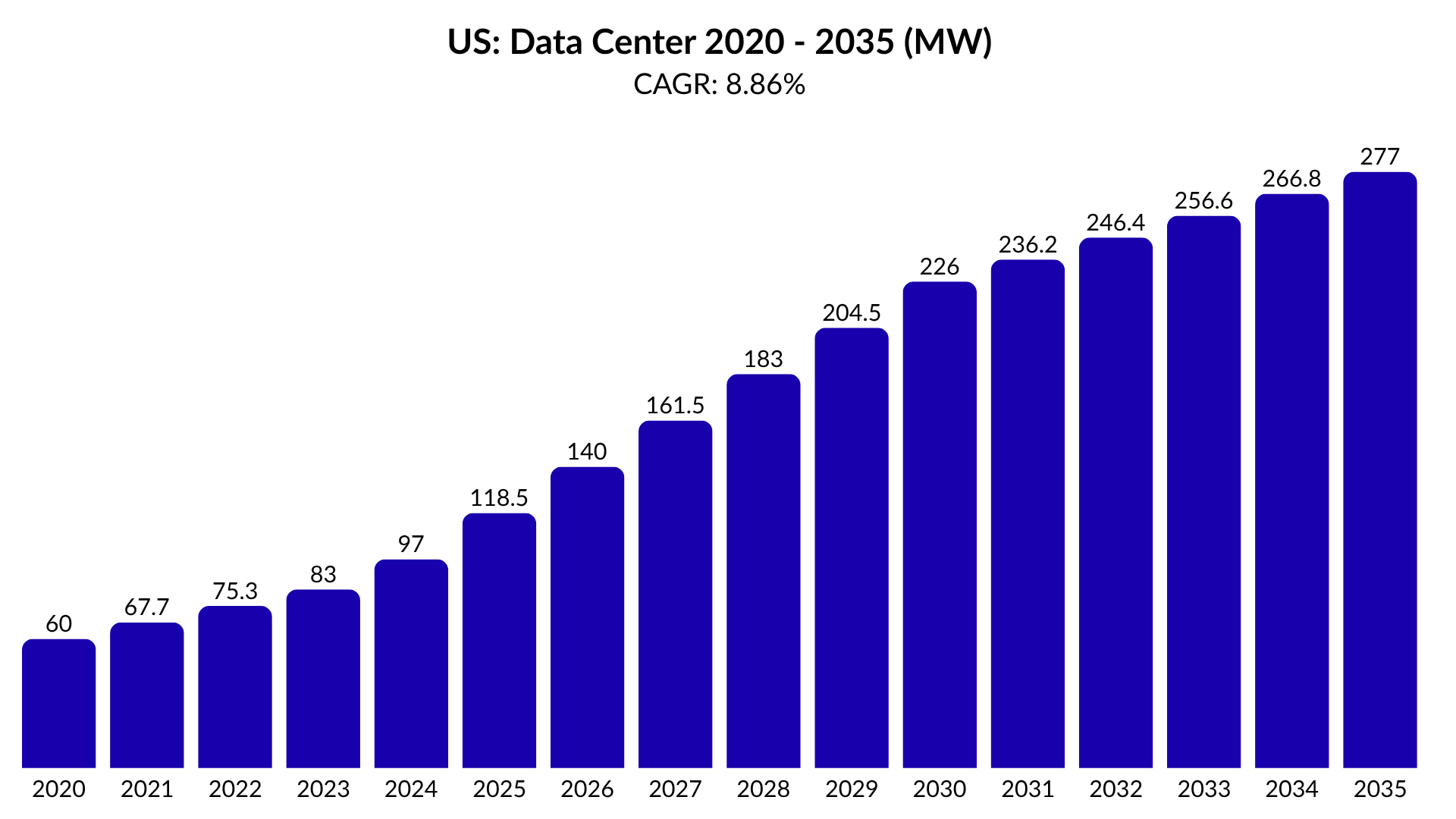

US data centre capacity is expanding at a scale rarely seen in modern infrastructure markets. Total capacity is projected to increase from 60 GW in 2020 to 277 GW by 2035, implying an 8.9% CAGR over fifteen years. The absolute scale of expansion matters more than the growth rate itself. Every additional layer of AI deployment increases demand for compute infrastructure, particularly hyperscale data centres supporting model training and inference workloads.

Source: EIA, US Department of Energy, NP Estimates

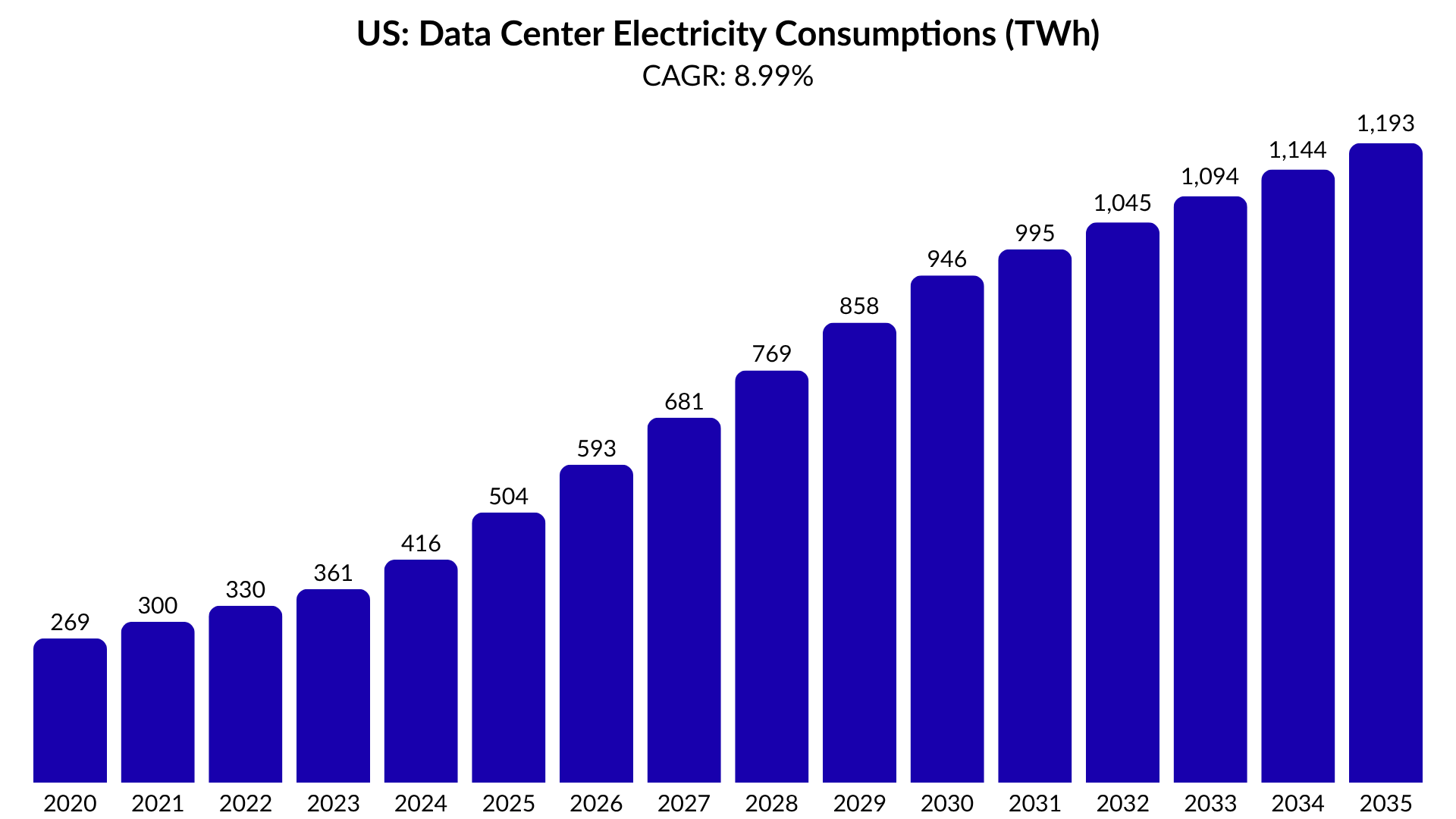

As AI deployment accelerates, the constraint increasingly shifts away from compute demand and toward electricity supply. US data centre electricity demand is projected to increase from 269 TWh in 2020 to 1,193 TWh by 2035, implying a 10.4% CAGR and a 4.4x increase over the period. The imbalance matters. Data centre capacity can scale relatively quickly through capital deployment, but electricity generation capacity cannot. Power plants require fuel supply stability and significantly longer construction timelines.

Part 3: Every AI Prompt Consumes Power

AI is creating a new source of energy demand growth within the US economy. While total US energy consumption historically increased by only 0.55% annually between 2015 and 2025, projected data centre expansion could materially accelerate demand growth over the next decade. The implication is significant because physical infrastructure typically expands far more slowly than digital infrastructure. As AI deployment scales further, energy availability may become a more important constraint than compute demand itself.

Source: EIA, US Department of Energy, NP Estimates

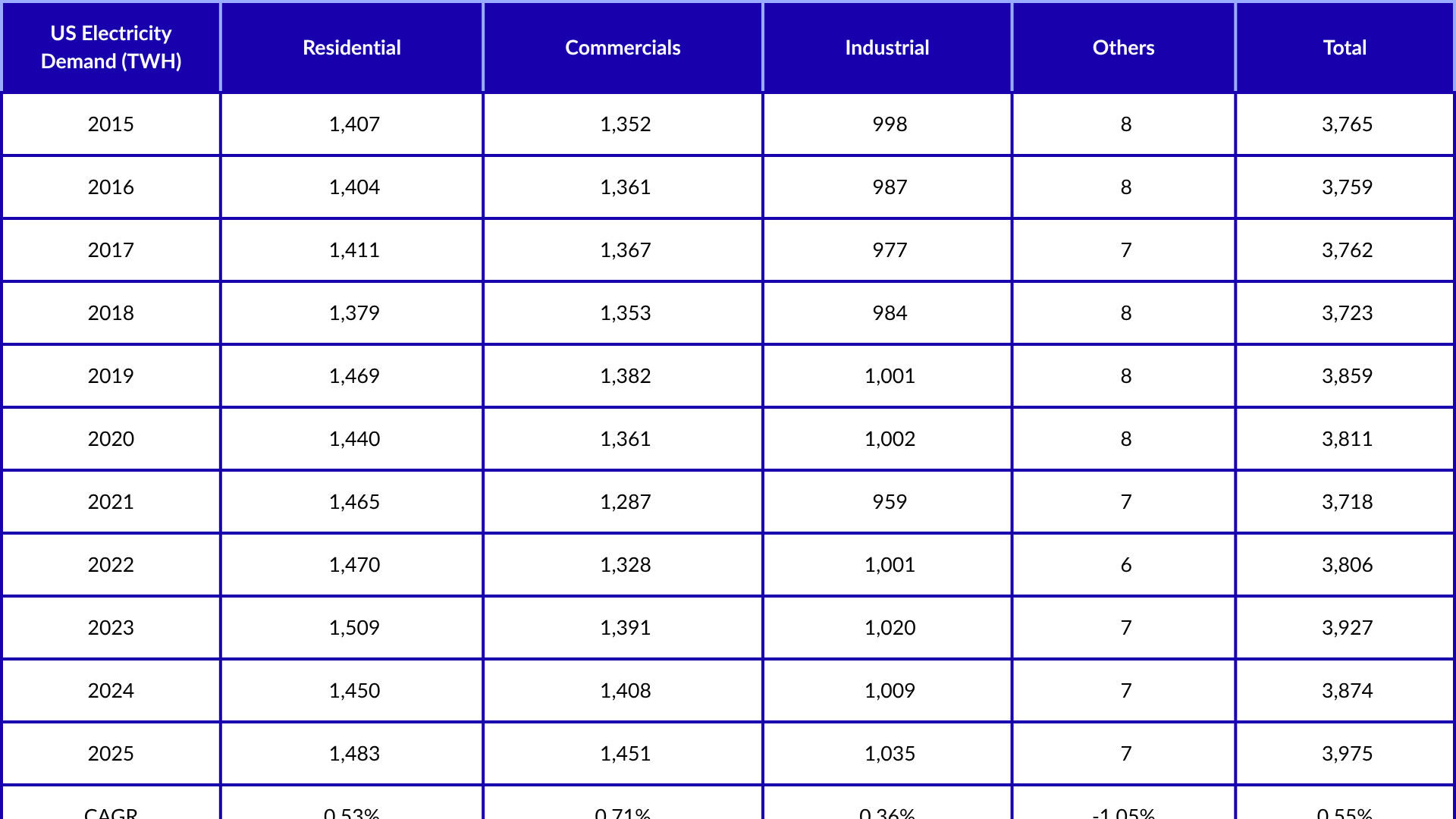

US electricity demand growth has historically been slow despite operating at enormous scale. Total electricity consumption increased from 3,765 TWh in 2015 to 3,975 TWh in 2025, implying only a 0.55% CAGR over the period. Residential electricity consumption increased from 1,407 TWh to 1,483 TWh, commercial demand from 1,352 TWh to 1,451 TWh, and industrial demand from 998 TWh to 1,035 TWh. Even the largest segment only expanded modestly over the last decade prior to the AI-driven data centre expansion cycle.

Source: EIA, US Department of Energy, NP Estimates

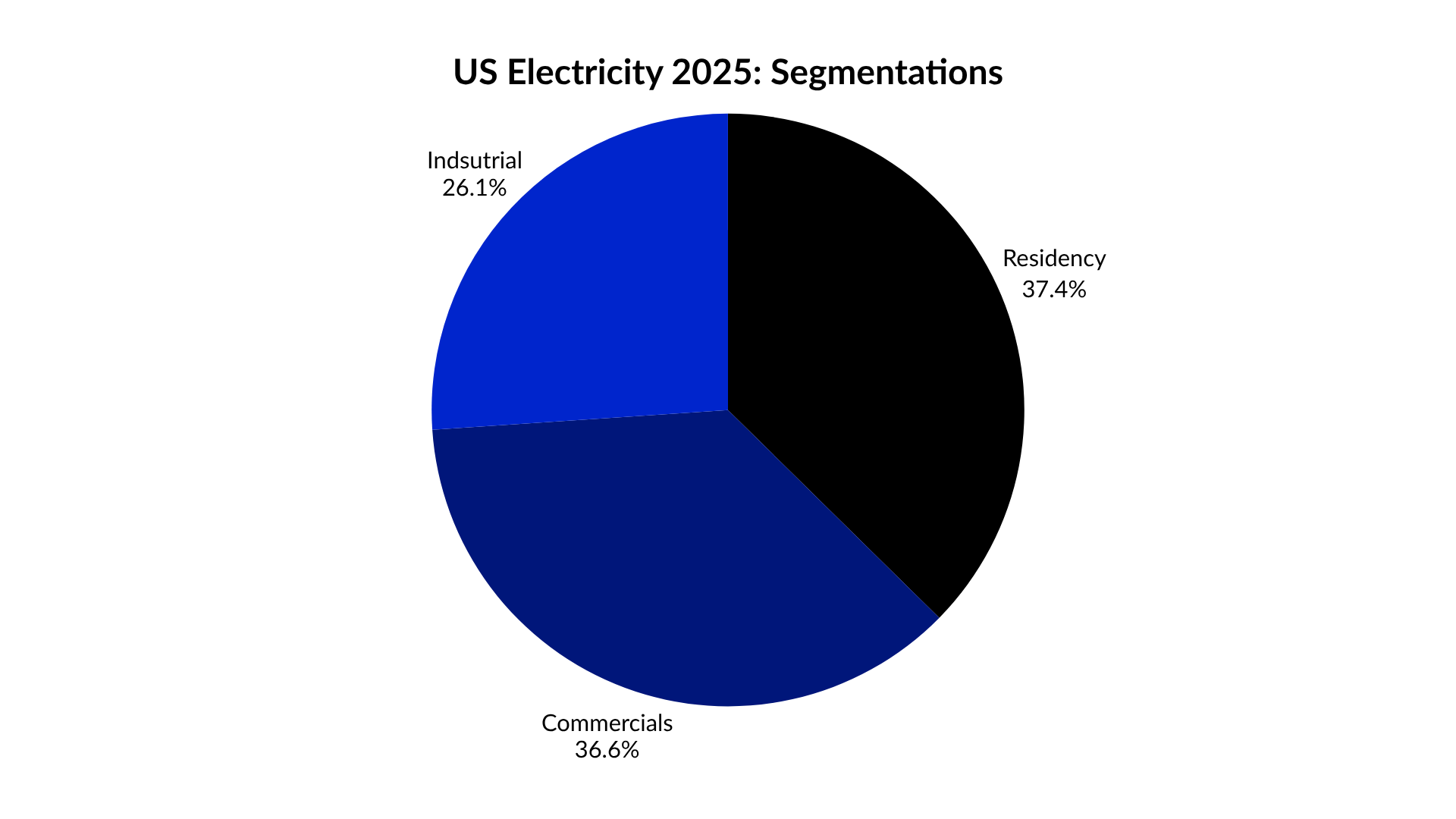

US energy demand is already heavily utilised across the economy. Residential demand accounts for 37.3% of total consumption, commercial demand 36.5%, and industrial demand 26.0%. Large-scale AI deployment therefore adds substantial new demand into a system already dominated by existing residential, commercial, and industrial consumption.

Source: NP Estimates

The significance of the increase lies in the change in growth expectations rather than the absolute level of demand itself. US energy consumption has historically expanded at a relatively modest pace, allowing generation capacity additions to remain broadly manageable. A sustained acceleration in demand growth would require a corresponding increase in generation and grid investment, creating new challenges for a power system that was not originally designed around rapid demand expansion.

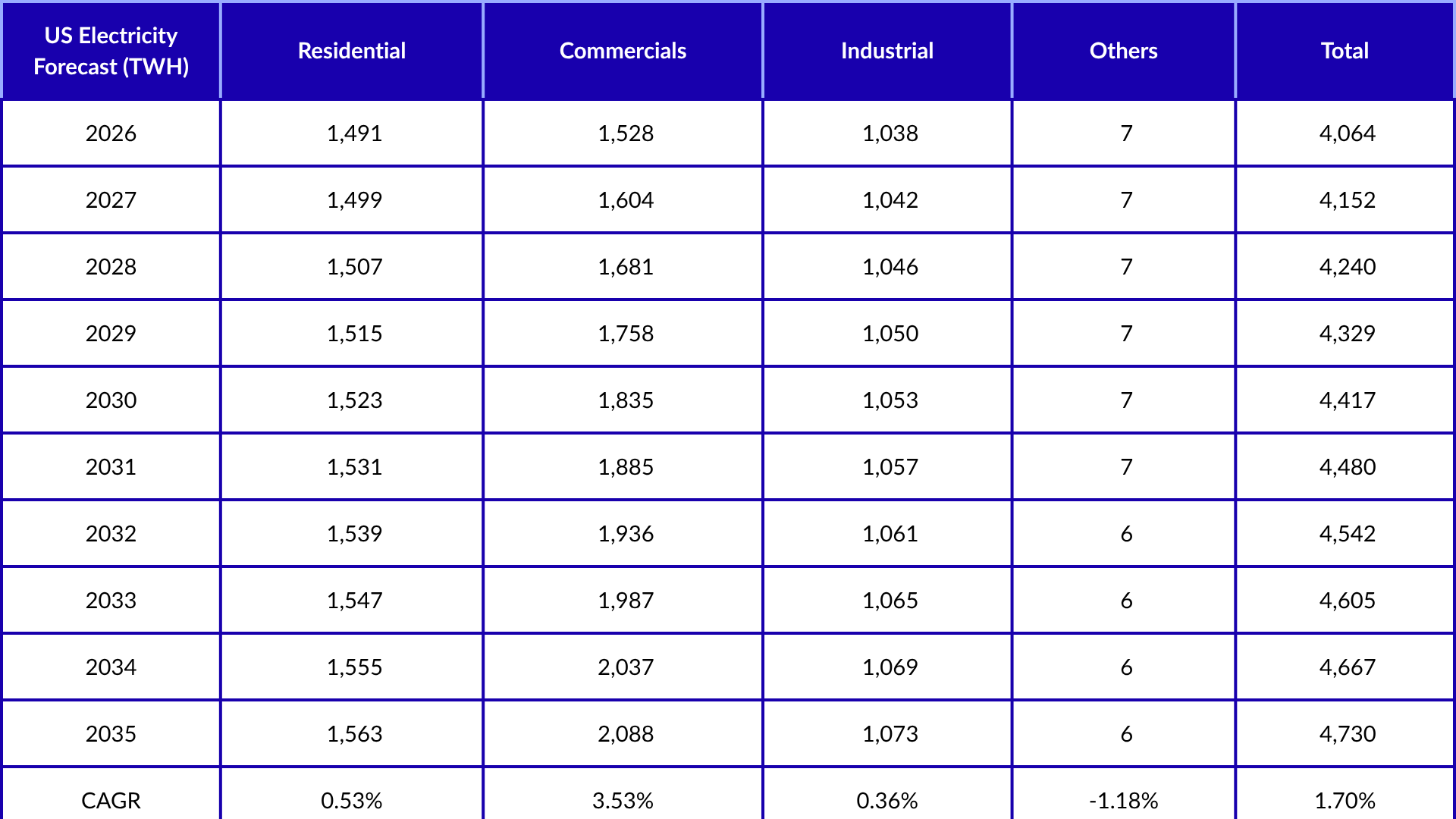

According to our estimations, US electricity demand growth materially accelerates once projected data centre expansion is included. Total electricity demand is forecasted to increase from 3,975 TWh in 2025 to 4,667 TWh by 2034, implying a 1.70% CAGR compared to the historical 0.55% growth rate. The increase is concentrated primarily within the commercial segment, where demand rises from 1,451 TWh to 2,037 TWh, implying a 3.53% CAGR versus the historical 0.71% trend. Data centres are expected to be the primary contributor behind the increase in commercial electricity demand. Under our estimations, the US power system would likely require generation capacity expansion above historical trends to maintain grid stability.

Source: NP Estimates

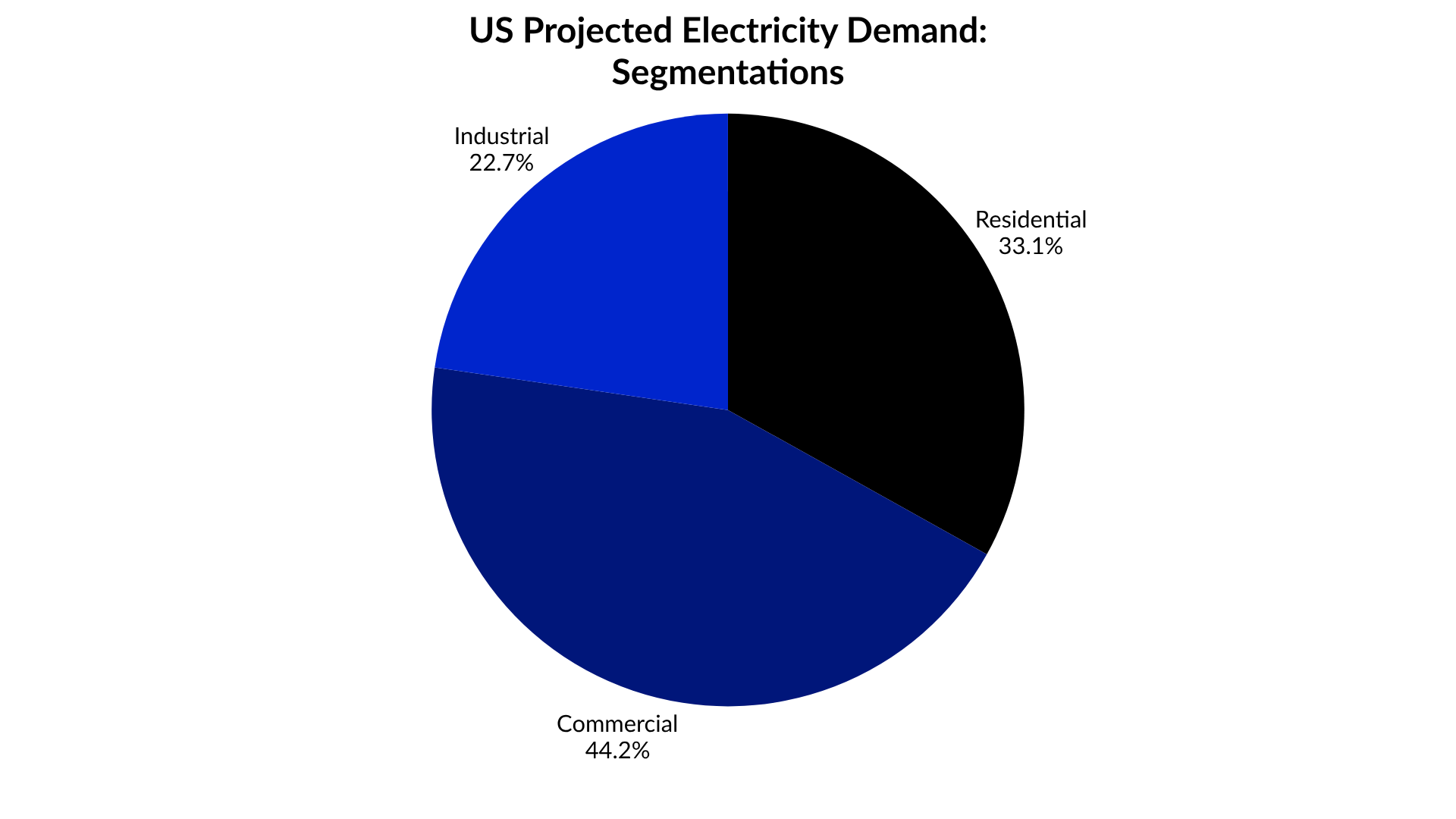

The demand shift becomes more visible by 2035. Commercial electricity consumption is projected to account for 44.14% of total US electricity demand, compared to 33.05% for residential and 22.67% for industrial demand. The increase is substantial considering commercial demand historically operated at levels relatively close to residential consumption. Under our estimations, data centres become one of the largest incremental electricity demand drivers within the US power system over the next decade.

The demand side of the equation is becoming increasingly visible. AI infrastructure expansion materially increases energy demand growth assumptions across the US power system. The larger issue now shifts toward supply expansion. We still view AI infrastructure growth as structurally sustainable over the long term. The question is no longer whether AI demand exists. The question is whether energy infrastructure can scale fast enough to support it.

Part 4: The Other Side of the Equation

Energy demand growth is only one side of the equation. While AI-driven data centre expansion could materially accelerate power consumption, expanding energy supply requires significantly longer development timelines and capital investment. The imbalance matters because demand can emerge relatively quickly, while generation capacity often takes years to build and integrate into the grid. Future AI growth therefore depends not only on technological progress, but also on the ability of the energy system to keep pace.

Source: EIA, US Department of Energy, NP Estimates

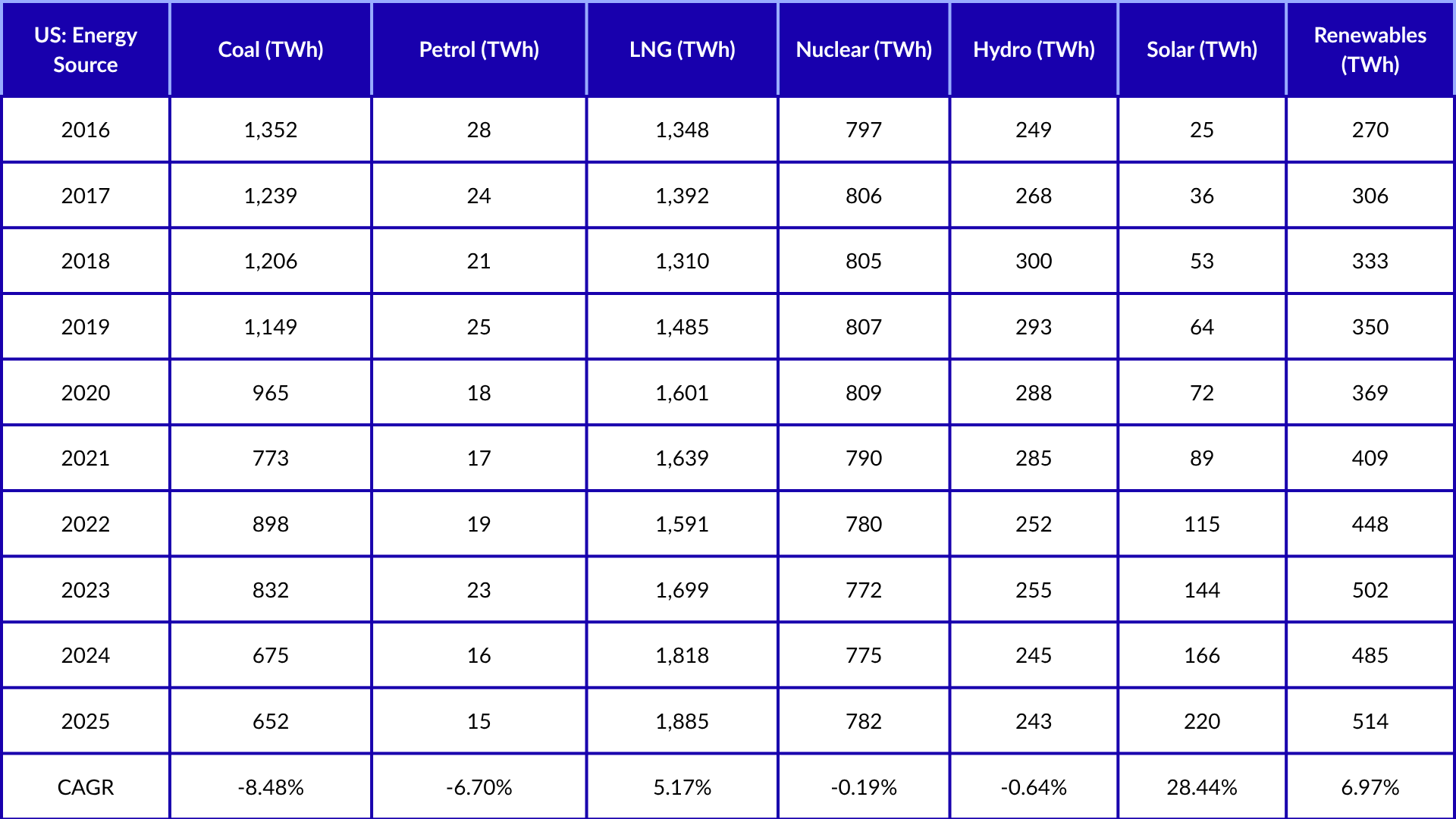

US energy generation is shifting away from coal and toward LNG and renewable energy sources. Coal generation declined from 1,582 TWh in 2015 to 652 TWh in 2025, implying an 8.48% annual decline over the period. Solar generation increased from 18 TWh to 220 TWh, representing approximately 28.44% annual growth, while broader renewable generation increased at roughly 6.97% annually. However, LNG remains the dominant source of incremental generation growth and currently serves as the primary source of dispatchable capacity supporting the US power system. LNG generation increased from 1,139 TWh in 2015 to 1,881 TWh in 2025, implying a 5.17% CAGR over the period.

Source: EIA, US Department of Energy, NP Estimates

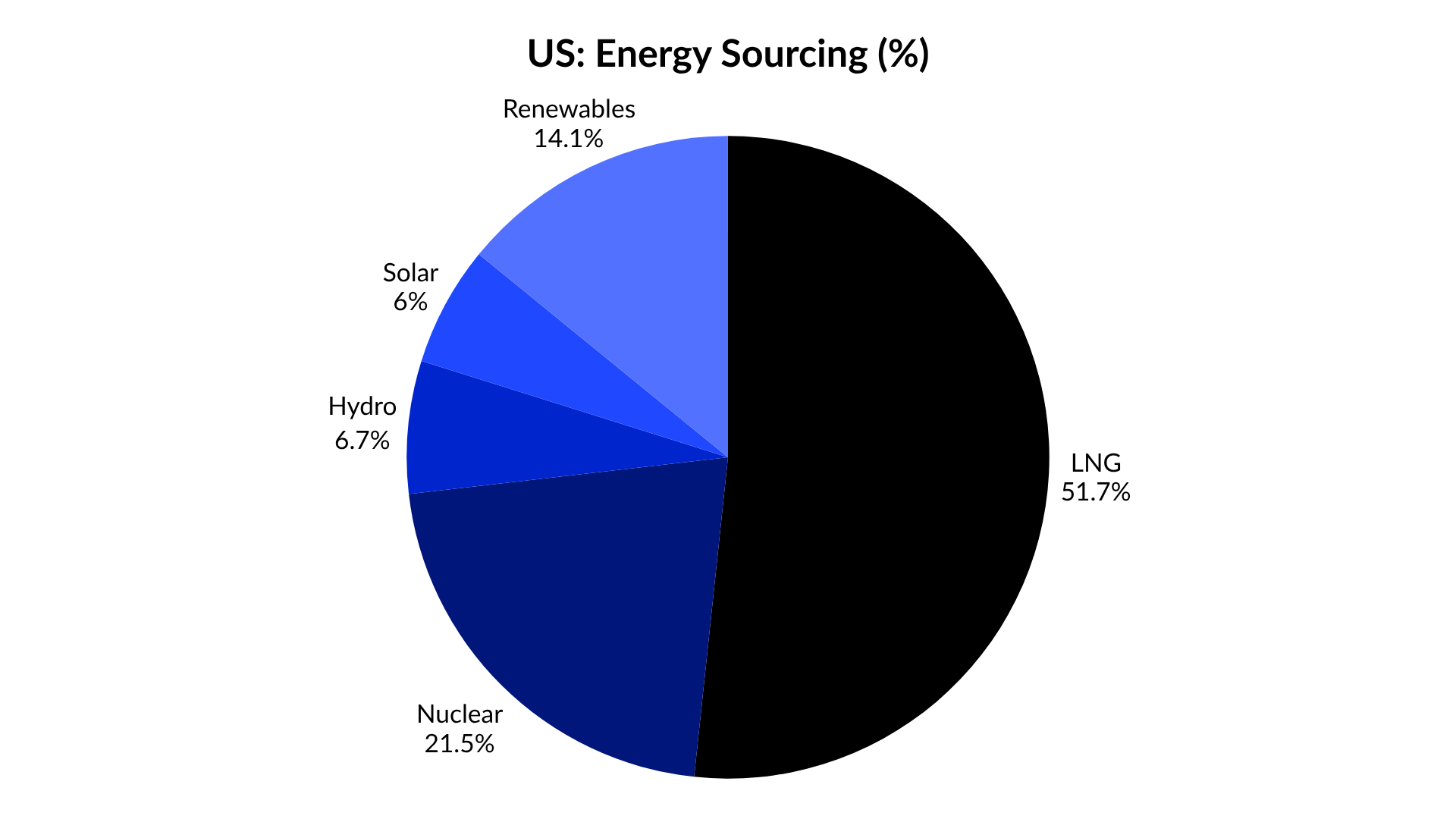

The composition matters because AI-related energy demand requires reliable and scalable power generation rather than intermittent capacity alone. LNG still accounts for 43.67% of total US electricity generation in 2025, materially larger than nuclear at 18.16%, renewables at 11.93%, hydro at 5.64%, and solar at 5.10%. The dependency matters because LNG pricing remains structurally more volatile than alternative baseload energy sources. Under our estimations, US energy demand growth could accelerate toward roughly 2% annually through 2035, driven primarily by data centre expansion. Incremental AI-related demand therefore increasingly ties US power stability and pricing exposure to LNG supply dynamics.

According to the New York Times, the current US administration already recognises the energy supply risk behind AI infrastructure expansion. Renewable energy alone may not scale fast enough to support rising electricity demand, while LNG dependency introduces fuel price volatility into the power system. The policy direction toward expanding domestic energy generation therefore appears structurally expected rather than politically surprising. Understanding future supply expansion requires evaluating not only energy sources, but also the economics and scalability of electricity generation itself.

Source: EIA, US Department of Energy, NP Estimates

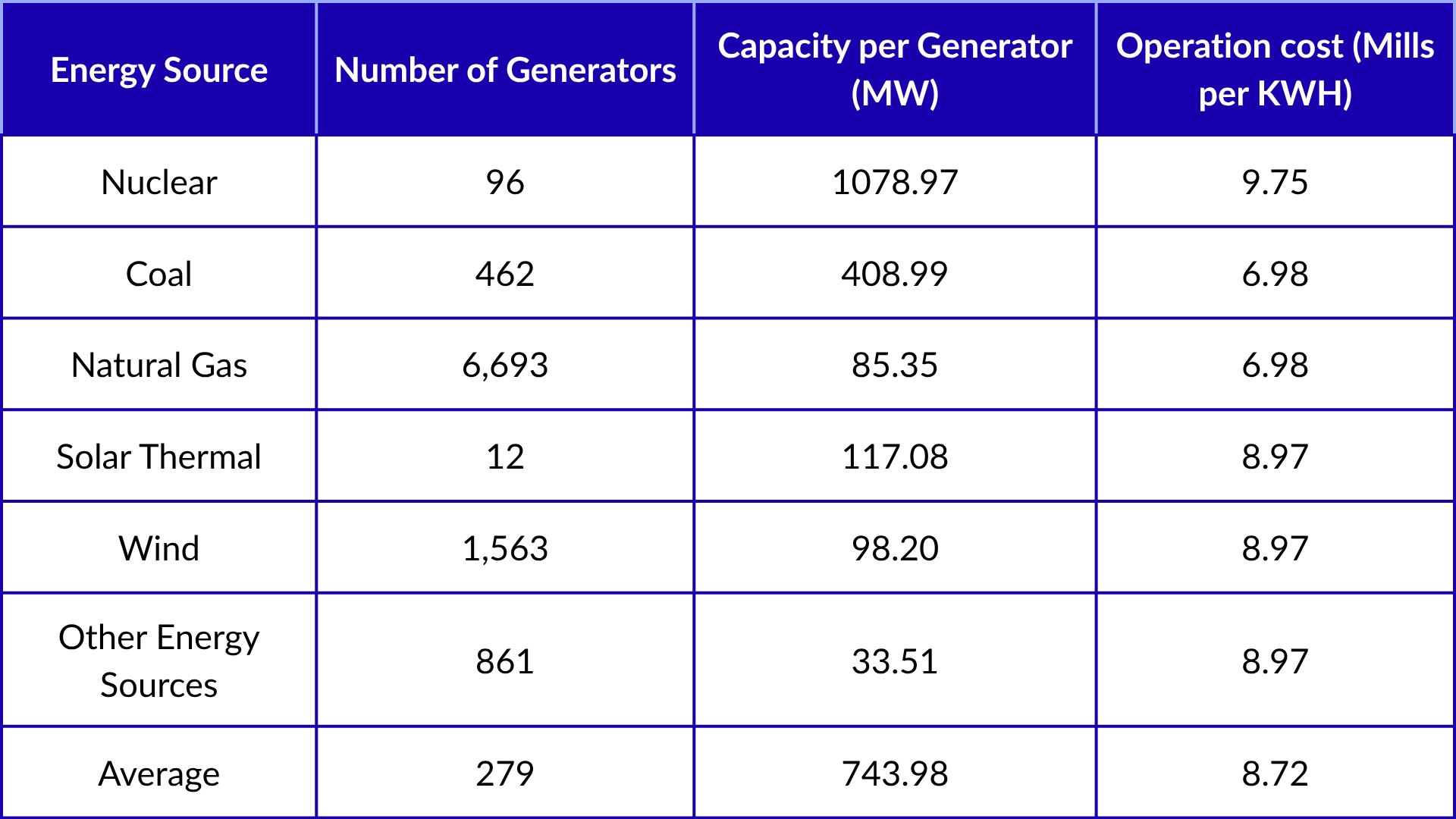

The US administration’s energy concerns are structurally understandable. Natural gas generators dominate the grid largely because they are easier and faster to deploy, but their average capacity per generator remains relatively low at around 85 MW. More importantly, LNG input costs remain exposed to commodity price volatility, creating instability in energy pricing during periods of rising demand. Nuclear generation solves part of the efficiency problem with average capacity reaching approximately 1,079 MW per generator, materially higher than any other major energy source. However, nuclear economics remains difficult due to extremely high upfront capital expenditure and elevated operating costs of roughly 9.75 mills per KWh. The result is visible in the deployment scale itself, with only 96 nuclear generators currently operating within the system.

Coal remains difficult to ignore despite the broader decarbonisation narrative. Coal generators operate at relatively low operating costs of approximately 6.98 mills per KWh while maintaining materially higher average generation capacity than LNG infrastructure. More importantly, coal generation is already deeply embedded within the existing US power system, making continued operation and incremental scaling comparatively easier from a cost and infrastructure perspective.

The challenge therefore becomes increasingly apparent. AI infrastructure expansion structurally increases energy demand, while large-scale renewable deployment remains constrained by intermittency, scale, and grid economics. Meeting future demand may ultimately require a combination of energy sources rather than reliance on any single technology.

Energy demand growth from data centres is economically positive for the power sector, but the optimal pathway for meeting that demand remains uncertain. The ability of the US energy system to expand reliably and economically may ultimately determine the pace of future AI deployment.

Part 5: The Second Order Effect

The AI investment thesis increasingly extends beyond artificial intelligence itself. While investors have largely focused on software, semiconductors, and data centres, the next phase of AI deployment may depend on the ability of the broader power system to support it. Building intelligence at scale ultimately requires electricity, and electricity requires generation capacity, fuel supply, transmission infrastructure, and long-term capital investment.

The implication is straightforward. AI demand is becoming easier to forecast than the infrastructure required to support it. The next decade may therefore be defined not only by advances in artificial intelligence, but also by the industries responsible for powering it. For investors, the question is no longer whether AI will continue growing. The more important question may be whether the underlying infrastructure can grow fast enough alongside it.

Editor's Take

The research above maps the infrastructure gap clearly. What it implies for private market investors is that the AI opportunity extends well beyond software and model companies. Power generation capacity, grid infrastructure, and data centre real estate are where a significant share of private capital is now moving, and many of the most interesting businesses in this space are still private.

Infrastructure has become one of the fastest-growing private asset classes for exactly this reason. The demand tailwinds described above, including data centre expansion, grid modernisation, and power generation buildout, map directly onto what institutional allocators are chasing in unlisted infrastructure strategies. The companies on the NonPublic platform, including Anthropic and others at the centre of the AI compute buildout, sit directly inside the demand curve this research describes.

For wholesale investors thinking about private market exposure, the second order question is worth taking seriously: not just which AI companies win, but which physical infrastructure they depend on, and whether that infrastructure is already investable today.

Edited by Chelsie Cay Zhu

This piece was researched and written by the NonPublic investment team. NonPublic Pty Ltd (ABN 49 607 216 928) holds Australian Financial Services Licence #482668. Investments are available to wholesale and sophisticated investors as defined under the Corporations Act 2001. This content is general in nature and does not constitute financial product advice. It does not take into account your objectives, financial situation, or needs. Investing in private markets involves significant risk, including the potential loss of your entire investment. Past performance is not a reliable indicator of future results. You should obtain independent financial advice before making any investment decision.

The Pre-IPO & Private Investment Marketplace for Australian Wholesale Investors

Book a free introduction call to learn how NonPublic can give you access to exclusive deals.

Book an Introduction Call